Steps in Preparation of Consolidated Financial Statements: Your Complete 2026 Guide

by Kevin Wiegand

|

Apr 18, 2026

|

Xero

Home

|

Xero

|

Steps in Preparation of Consolidated Financial Statements: Your Complete 2026 Guide

You are staring at spreadsheets from eight different Xero entities, trying to eliminate intercompany transactions while the board pack is due in three days. Your balance sheet will not balance. Eliminations do not reconcile. Month-end has stretched into a second week. Preparing consolidated financial statements should not take this long or leave you second-guessing the numbers. This guide walks you through the steps in preparation of consolidated financial statements and the practical ways to cut the manual grind.

Steps in Preparation of Consolidated Financial Statements

Seven steps in preparation of consolidated financial statements turn entity-level financial data into one set of group reports. The process starts with identifying controlled subsidiaries, then moves through Trial Balance collection, policy alignment, foreign currency translation under IAS 21, intercompany eliminations, non-controlling interest adjustments, statement aggregation, and final review and disclosure. Under IFRS 10, consolidation is based on control, not just ownership percentage, so the process starts with identifying every controlled entity before any aggregation begins.

Ready to Automate Your Financial Consolidation?

Stop wrestling with manual consolidations and broken formulas. dataSights automates multi-entity reporting, Xero consolidations, and Power BI connections. Join 300+ businesses already transforming their financial reporting with our platform, rated 5.0 out of 5 by 90+ verified Xero users.

Consolidated financial statements present your parent company and all subsidiaries as a single economic entity. They give investors, lenders, and regulators a complete view of your group’s financial position.

Who Needs to Prepare Consolidated Statements

IFRS 10 requires consolidation when the parent controls an investee. Control exists when you have power over the investee’s relevant activities, you are exposed or have rights to variable returns, and you can use that power to affect those returns. Ownership of more than 50% often indicates control, but it is not the test. Where the parent has significant influence but not control (usually 20% or more), the investment is accounted for using the equity method under IAS 28 rather than full consolidation.

Your group needs consolidation if you operate multiple legal entities, own subsidiaries in different countries, or manage holding company structures. Even businesses with just two entities benefit from consolidated reporting.

Regulatory Context: IFRS, US GAAP, and Jurisdictional Reliefs

For UK groups, the legal requirement to prepare group accounts sits alongside your reporting framework. In practice, UK-adopted IFRS and FRS 102 follow similar consolidation principles, but differ in areas such as goodwill treatment and some exclusion criteria, so always assess both the legal and framework-specific rules.

Consolidated vs Combined vs Equity Method

Finance teams often confuse these three approaches. The right method depends on the level of control or influence your parent company has over each entity.

Method

When to Use

Key Feature

Full consolidation

Parent controls subsidiary (typically >50%)

100% of assets/liabilities; NCI shown separately

Equity method

Significant influence, not control (20-50%)

Single line item; adjust for share of profit/loss

Combined statements

Common ownership, no parent-subsidiary relationship

Practice is jurisdiction-specific; intercompany balances are often still eliminated to avoid overstatement

Combined statements are not defined in IFRS, so presentation depends on purpose and jurisdiction. Policies should be disclosed clearly.

Under IFRS 11 joint arrangements, joint ventures use the equity method. Proportionate consolidation is not permitted for joint ventures under IFRS.

Pre-Consolidation Checklist: What You Need Before You Start

Consolidation accuracy depends on input quality. Before the seven-step process, verify:

A documented list of all entities in scope with incorporation dates, ownership percentages, and business activities

An aligned group chart of accounts with a mapping table from local to group-level accounts

Clean, finalised trial balances from every entity with all local adjustments posted

Agreed intercompany identification rules – tag transactions at entry, not at period-end

A defined currency translation approach with documented rate sources

Confirmed consolidation method for each entity (full consolidation under IFRS 10 or equity method under IAS 28), plus a separate assessment of whether any exemption from preparing consolidated financial statements applies

Submission deadlines and a clear sign-off workflow

Be careful with exclusions. Under IFRS, exclusions are narrow and usually tied to specific parent exemptions or investment-entity treatment, while FRS 102 may allow some additional exclusions in limited cases.

Skipping this preparation turns a two-day consolidation into a two-week clean-up. The Xero consolidation platform keeps trial balances current and configures chart of accounts mapping once.

Framework note: This guide primarily references International Financial Reporting Standards (IFRS 10, IFRS 3, IAS 21, IAS 36) because most UK listed and larger groups apply UK-adopted IFRS. UK groups using FRS 102 follow similar consolidation principles, but some areas differ, including NCI measurement, goodwill treatment, and exclusion criteria. The Companies Act 2006 legal requirements apply regardless of your chosen accounting framework.

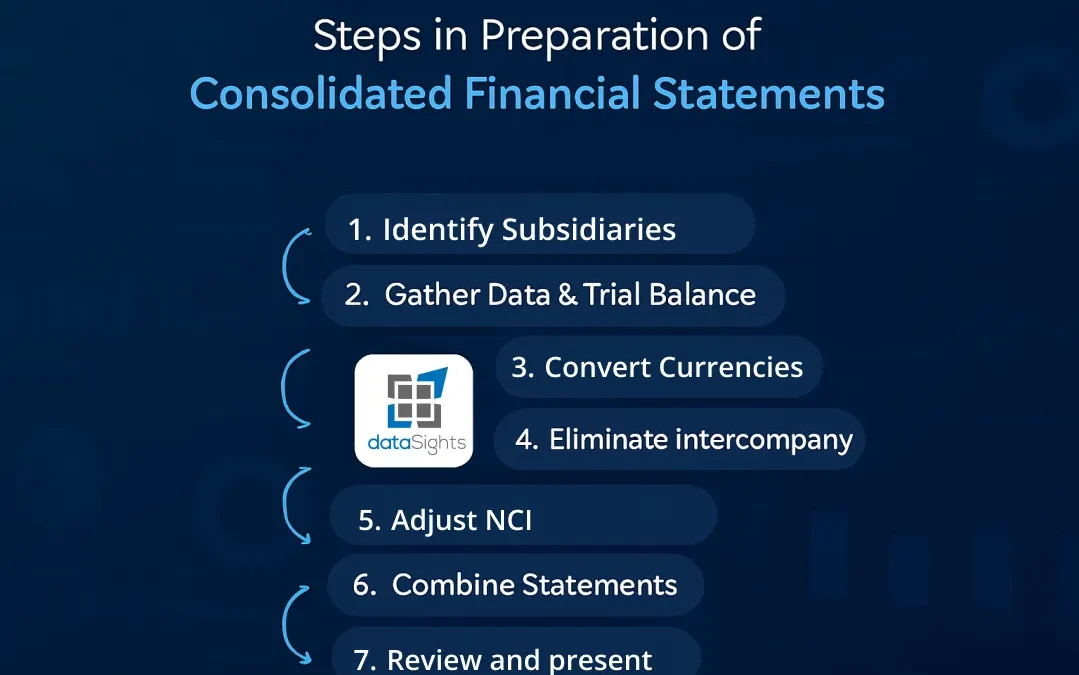

The Seven Steps in Preparation of Consolidated Financial Statements

Each step addresses a specific consolidation requirement, from determining which entities belong in your group to presenting final statements to stakeholders. The process starts with Trial Balance data from every entity, moves through account standardisation, currency translation, and intercompany elimination, then aggregates everything into consolidated reports that reconcile back to source systems.

Step 1: Identify Subsidiaries and Determine Control

Before consolidating, determine exactly which entities belong in your group.

Defining Control and Ownership Thresholds

IFRS 10 explains control as requiring three linked conditions:

Power over the investee

Exposure or rights to variable returns

Ability to use that power to affect those returns

Majority ownership often indicates control, but it is neither required nor sufficient on its own.

Under US GAAP (ASC 810), some entities are assessed under the VIE model. The entity that is the primary beneficiary (power plus economics) consolidates the VIE. Document each subsidiary’s incorporation date, ownership percentage, and business activities. This creates your consolidation scope.

Structured Entities (IFRS) and VIEs (US GAAP)

IFRS uses the term structured entity for arrangements where voting rights are not the dominant control factor; related disclosures are in IFRS 12. US GAAP uses the comparable variable interest entity (VIE) concept. IFRS reporters assess control and structured-entity disclosures; US GAAP reporters perform the VIE analysis.

Step 2: Gather, Align, and Standardise Financial Data

Data collection is where consolidation lives or dies.

Trial Balance as Your Foundation

Trial Balance is the definitive report for multi-entity consolidation. Pull complete Trial Balance data from each entity to guarantee your consolidation ties back to source systems. Without accurate Trial Balance data, your consolidated balance sheet will not reconcile. Verify every account before consolidation begins.

Mapping to a Group Chart of Accounts

Each entity may use its own local chart of accounts. Before you can add balances line by line, map every local account to your group-level chart:

Create a master mapping table linking each local account code to its group equivalent

Identify unmapped accounts and assign them to the correct group category

Validate by running a test aggregation and checking for anomalies

Standardise account structures once and reuse the mapping each period.

Ensuring Consistent Accounting Policies

All entities must use consistent accounting policies. Review depreciation methods, revenue recognition policies, and inventory valuation approaches across all subsidiaries. Adjust subsidiary figures where policies differ from the parent (IFRS 10).

Handling Different Reporting Periods

If a subsidiary’s reporting date differs from the parent’s, IFRS 10 allows a gap of up to three months when aligning dates is impracticable. You must adjust for significant transactions and events in the intervening period. In practice, most groups still aim to align reporting dates wherever possible.

Watch how dataSights automates the complete consolidation workflow, from data gathering through final statement generation.

Step 3: Convert Foreign Currency Translations

Multi-currency groups face an additional step. Each subsidiary first records transactions in its functional currency, which is the currency of its primary economic environment. You then translate those results into the group’s presentation currency under IAS 21 for consolidation:

Assets and liabilities: Translate at the closing rate on the reporting date

Income and expenses: Translate at transaction-date rates (or an average rate for the period where it is a reasonable approximation)

Equity items: Keep at historical rates

Net difference: Recognise in OCI as a cumulative translation adjustment (CTA), reclassified to profit or loss on disposal of the foreign operation

For example, a US subsidiary with $1m of revenue translated at an average rate of £0.79 becomes £790,000. If it has $500,000 of assets translated at a closing rate of £0.81, those assets become £405,000. The translation difference goes to the foreign currency translation reserve in equity through OCI.

Document your rate sources and methodology. Use closing rates for balance sheet items and average rates for income statement items consistently. Record rates applied for each entity so the audit trail is complete. For multi-currency groups, consolidation software handles rate application automatically.

Step 4: Eliminate Intercompany Transactions

Intercompany transactions create artificial profits that do not reflect the group’s true position.

Types of Intercompany Transactions to Eliminate

Common eliminations include intercompany sales and purchases, loans and interest, dividends between entities, management fees, and asset transfers. The group should show transactions with external parties only. For elimination journal entry detail, see the elimination entries guide.

Intercompany Matching Before Elimination

Before posting elimination entries, match intercompany balances between entities. If Entity A records a receivable of 50,000 from Entity B, Entity B should have a corresponding payable of 50,000. Any mismatch needs investigation before elimination. Tag intercompany transactions at the point of entry – not at period-end – so matching is straightforward.

Upstream, Downstream, and Lateral Transactions

Downstream transactions flow from parent to subsidiary. Upstream transactions go from subsidiary to parent. Lateral transactions occur between two subsidiaries of the same parent. All three types require elimination. The direction affects how you allocate the elimination between controlling and non-controlling interests.

Unrealised Profit Elimination

If one entity sells inventory to another and that inventory remains unsold at period-end, the profit is unrealised. Calculate unrealised profit by identifying intercompany markup on goods still held within the group. Eliminate from both closing inventory and profit figures. Defer profit until sale to third parties and adjust the carrying amount to cost to the group. Consider deferred tax effects (IAS 12).

For example, Parent sells inventory to Subsidiary for £50,000 at a £10,000 profit. If the stock remains unsold at year-end, remove the £50,000 intercompany sale and eliminate the £10,000 unrealised profit from inventory and group profit.

Intra-Group Cash Flow Elimination

Also eliminate intercompany dividends (and related investment income) and intercompany interest income/expense together with the underlying receivable/payable. In the consolidated cash flow, eliminate all intra-group cash flows.

Why Eliminations Are the Hard Part

Manual eliminations are time-consuming and error-prone, often without a complete audit trail. System-based rules provide repeatability, documentation, and drill-down capability. IFRS 10 requires eliminating all intragroup balances, transactions, income, and expenses in full.

Note for Xero users: Xero supports multi-entity connections and report exports, but complex group eliminations typically require an added consolidation or reporting layer to manage matching, posting, and audit trails at scale.

Step 5: Adjust for Non-Controlling Interests (NCI)

When you own less than 100% of a subsidiary, you must account for the portion you do not own.

Non-Controlling Interests (NCI)

NCI represents equity not attributable to the parent. At acquisition, IFRS 3 permits measuring NCI at fair value (full goodwill method) or at its proportionate share of the acquiree’s identifiable net assets (partial goodwill method). In subsequent periods, attribute profit or loss and OCI between the parent and NCI.

For UK groups using FRS 102, the acquisition-date NCI measurement approach differs from IFRS, so check your framework before calculating goodwill.

NCI in Balance Sheet and Income Statement

In the income statement, allocate based on ownership percentages. If you own 80% of a subsidiary and its profit after eliminations is 100,000, 20,000 is attributed to NCI. On the balance sheet, NCI increases with its share of profits and decreases with losses or dividends.

Downstream (parent to subsidiary) eliminations adjust the parent’s profit with no impact on NCI. Upstream (subsidiary to parent) eliminations reduce the subsidiary’s profit, so NCI’s share decreases accordingly.

Step 6: Combine Financial Statements

Aggregate all adjusted entity data into unified group statements.

Aggregating Assets, Liabilities, and Equity

Combine assets, liabilities, equity, revenues, and expenses across all entities line by line. The parent’s investment in subsidiaries is eliminated and replaced with the underlying net assets plus goodwill.

Produce a statement of financial position, statement of profit or loss and OCI, statement of changes in equity, statement of cash flows, and notes with accounting policies and disclosures.

Goodwill and Investment Elimination

On first-time consolidation, eliminate the parent’s investment against the subsidiary’s identifiable net assets:

Calculate goodwill as consideration transferred, plus the fair value of any non-controlling interest, plus the fair value of any previously held interest in the subsidiary, less the acquisition-date fair value of identifiable net assets

Recognise under IFRS 3/ASC 805 in the consolidation layer

Test annually for impairment under IAS 36 (not amortised under IFRS)

For foreign operations, translate goodwill at the closing rate

Example: Parent pays £800,000 for 80% of a subsidiary whose identifiable net assets are fairly valued at £750,000. If the fair value of the remaining 20% NCI is £200,000, goodwill is £250,000 (£800,000 + £200,000 – £750,000).

Under IFRS, test goodwill annually for impairment under IAS 36. Under FRS 102, goodwill is generally amortised over its useful economic life. Xero does not track goodwill – post this adjustment in your consolidation layer.

Preparing Consolidated Income Statement

Combine all revenues and expenses. Eliminate intercompany revenue and expenses. Allocate net income between the parent and NCI.

Preparing Consolidated Balance Sheet

Add assets and liabilities line by line. Eliminate intercompany balances. Show NCI as a separate equity component.

Preparing Consolidated Cash Flow Statement

Show cash activities from operations, investments, and financing for the entire group. Eliminate intra-group cash transfers.

Step 7: Review, Audit, and Present

Consolidation is not complete until you verify every number and prepare disclosures.

Final Reconciliation Checks

Verify that:

All intercompany balances eliminate to zero

Trial Balance reconciles to consolidated statements

NCI calculations are correct

Currency translations are accurate

Run variance analysis against prior periods and budgets.

Post Group-Level Adjustments

Post any consolidated-level journal entries: group accruals, reclassifications, audit-driven corrections, and fair value adjustments from acquisition. Track these separately from local books.

Maintain audit logs showing who made each adjustment, when, and why. Document all elimination entries with supporting schedules. financial consolidation reporting through automation creates timestamped, user-identified audit trails that manual processes cannot match.

Stakeholder Presentation

Present consolidated statements to investors, lenders, and regulators. Include disclosures about consolidation methods, eliminations, and NCI. Add management commentary on variances and performance drivers.

Continuous vs Period-End Consolidation

Spreadsheet consolidation produces a point-in-time snapshot, so issues surface after the close. With continuous consolidation, mismatches are visible during the month, when they are easier to investigate and fix.

Common Challenges in Manual Consolidation

Manual consolidation creates the same problems in every finance team that relies on spreadsheets.

1. Cascading Data Entry Errors

A miskeyed balance in a subsidiary trial balance throws off your eliminations, your NCI allocation, and your consolidated P&L. You may not find the error until the board pack is already late. With no validation layer between the source data and your consolidated output, one wrong figure in one entity cascades through the entire group.

2. Intercompany Reconciliation Bottlenecks

Matching receivables to payables across eight or ten entities, chasing down mismatches, and rebuilding elimination entries from scratch each period – these tasks consume days your team does not have. When reporting deadlines are tight, intercompany reconciliation is the bottleneck that pushes month-end into a second week.

3. No Audit Trail

Spreadsheets leave your group exposed. No record shows who changed a formula, when they changed it, or why. If an auditor asks you to trace an elimination back to its source transaction, you are rebuilding the logic manually. This is the gap that financial consolidation reporting through automation closes – every adjustment is timestamped and user-identified.

4. The Automation Gap

Most finance teams do not struggle because they lack software. They struggle because manual work still sits between entity close and group reporting. Intercompany matching, elimination journals, FX checks, and last-minute reclasses create delay and error risk even after teams invest in tooling.

How Automation Transforms the Consolidation Process

Modern consolidation does not require weeks of manual work.

dataSights delivers pre-formatted Management Reports through its web platform, including:

Consolidated P&L

Balance Sheet

Trial Balance

AR/AP detail

Budget variance

Cash flow

For teams that prefer spreadsheets, Excel automation keeps live consolidated data ready to use without CSV exports. Power BI remains available for deeper drill-down analysis and custom dashboards. Behind the scenes, data syncs from multiple Xero entities via API into a central reporting layer, so reports stay current without manual exports.

Consolidate both small and large entities simultaneously. Automated elimination rules run with full audit trails. With continuous consolidation, issues surface daily instead of two weeks after month-end.

Gartner predicts that finance teams using cloud ERP applications with embedded AI will achieve a 30% faster financial close by 2028, with AI-enabled cloud ERP spending projected to reach 62% by 2027, up from 14% in 2024.

From Consolidation to Management Reporting

Accurate consolidation is only the starting point. Finance teams also need board-ready management packs that show consolidated P&L, Balance Sheet, Trial Balance, budget variance, AR/AP detail, and commentary on group performance. When consolidation ties back to entity Trial Balances and elimination logic is documented, management reporting becomes faster, more defensible, and easier to explain to directors and auditors.

Frequently Asked Questions

Manual consolidation can take anywhere from a few days to a few weeks, depending on group complexity, data quality, intercompany mismatches, and how many group-level adjustments are needed. Many finance teams reduce month-end close from over 15 days to under 5 once Trial Balance collection, eliminations, and reporting are automated, but actual results vary by process maturity and entity structure.

Yes. Consolidation software can automate Trial Balance collection, chart of accounts mapping, currency translation, intercompany eliminations, and management reporting. Look for a solution that gives you board-ready Management Reports first, with Excel automation and Power BI connectivity available where your team needs them, plus clear audit trails and multi-currency support.

The Trial Balance is the foundation of consolidation. It provides the complete, reconciled account balances from each entity that feed group reporting. If your consolidated figures do not tie back to entity Trial Balances, you cannot be confident in the result.

The most common mistakes are incomplete intercompany matching, inconsistent accounting policies, missing unrealised profit eliminations, incorrect FX rates, weak chart of accounts mapping, and overlooked group-level adjustments such as goodwill or non-controlling interest. A structured checklist and automated validation reduce these risks significantly.

IFRS allows a reporting date difference of up to three months when alignment is impracticable, provided you adjust for significant transactions and events in the intervening period. Where possible, align reporting dates to reduce consolidation complexity and review work.

Before consolidation, each subsidiary’s results should be adjusted to align with the parent’s reporting framework and accounting policies. Groups using IFRS and groups using FRS 102 follow similar core consolidation principles, but some details differ, including goodwill treatment, non-controlling interest measurement, and some exclusion rules.

Full consolidation includes 100% of a controlled subsidiary’s assets, liabilities, income, and expenses, with non-controlling interest shown separately where the parent owns less than 100%. Under IFRS, joint ventures are generally accounted for using the equity method, so proportionate consolidation is not permitted for those arrangements.

Associates and joint ventures are usually accounted for using the equity method rather than full consolidation. Instead of combining all assets, liabilities, income, and expenses line by line, you show a single investment line and your share of profit or loss.

Yes, if you control that subsidiary. Consolidation is based on control, not on how many subsidiaries you have, so a parent with one controlled subsidiary may still need to prepare consolidated financial statements unless a valid exemption applies.

Consolidated financial statements present a parent and its controlled subsidiaries as a single economic entity, with intercompany transactions eliminated and non-controlling interests shown separately where relevant. Combined financial statements present entities together without a parent-subsidiary structure. The treatment is jurisdiction-specific, and intercompany balances may still be eliminated depending on the purpose of the presentation and the accounting policy used.

A complete set typically includes a statement of financial position, a statement of profit or loss and other comprehensive income, a statement of changes in equity, a statement of cash flows, and notes, including significant accounting policies and required disclosures.

Exemptions depend on both the legal regime and the reporting framework. In the UK, some small groups and some subsidiaries included in higher-level group accounts may qualify for exemption, but the conditions are specific and should be checked carefully against the current legal and accounting requirements.

Your Path to Faster, More Accurate Consolidation

Preparing consolidated financial statements does not have to consume weeks of your finance team’s time. The seven-step process is well established, but manual execution creates bottlenecks, errors, and stress. Start with clean Trial Balance data, standardise your chart of accounts, and automate eliminations. Continuous consolidation gives visibility throughout the month, not just at period-end. Your consolidated statements become reliable management tools rather than period-end ordeals.

Transform Your Financial Consolidation Process Today

Ready to cut your month-end close from weeks to days? dataSights automates multi-entity reporting with board-ready Management Reports, Trial Balance-based consolidation, and fully documented elimination entries. Teams that prefer Excel can work with live, refreshed data there too, while Power BI is available for deeper drill-down analysis. Rated 5.0 by 80+ Xero users and trusted by 300+ businesses, dataSights gives finance teams a faster, more reliable way to close and report.

I’m Kevin Wiegand, and with over 25 years of experience in software development and financial data automation, I’ve honed my skills and knowledge in building enterprise-grade solutions for complex consolidation and reporting challenges. My journey includes developing custom solutions for data teams at Gazprom Marketing & Trading and E.ON, before founding dataSights in 2016. Today, dataSights helps over 250 businesses achieve 100% report automation. I’m passionate about sharing my expertise to help CFOs and Financial Controllers reduce their month-end close time and eliminate the manual Excel exports that drain their teams’ valuable time.