You’re facing another month-end close, staring at spreadsheets from multiple entities that need consolidating, and wondering if there’s a better way than the manual Excel marathon ahead. Financial consolidation doesn’t have to consume weeks of your team’s time or leave you second-guessing whether eliminations balance. Whether you’re managing a handful of subsidiaries or consolidating across dozens of entities, the process follows the same basic principles – you just need the right approach and tools to execute it efficiently. This guide walks you through exactly how to consolidate financial statements, from gathering Trial Balances to producing board-ready reports that actually reconcile.

How To Consolidate Financial Statements

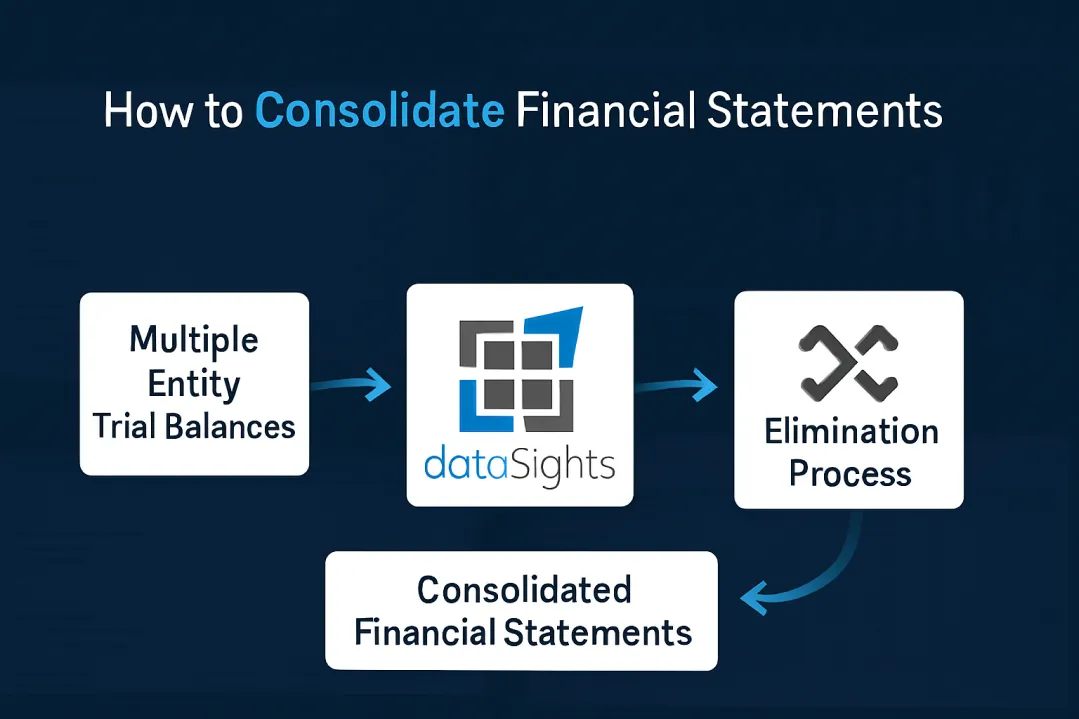

Knowing how to consolidate financial statements means gathering Trial Balance data from all entities, eliminating intercompany transactions, adjusting for non-controlling interests, and combining the remaining balances into unified reports. The process typically takes 10 or more days to complete manually, but with automated consolidation software like dataSights, CFOs reduce this to under 5 days.

Ready to Automate Your Financial Consolidation?

Stop wrestling with manual consolidations and broken formulas. dataSights automates multi-entity reporting, Xero consolidations, and Power BI connections. Join 300+ businesses already transforming their financial reporting with our platform, rated 5.0 out of 5 by 77+ verified Xero users.

Table of Contents

Understanding the Foundation: What Are Consolidated Financial Statements?

Consolidated financial statements present your parent company and subsidiaries as a single economic entity. Think of it as creating one unified financial picture from multiple separate pieces – combining assets, liabilities, revenue, and expenses while removing any internal transactions that would otherwise inflate your numbers.

Under IFRS 10, you consolidate when you control another entity—meaning you have power over relevant activities, exposure to variable returns, and the ability to affect those returns through your power. “Significant influence” (IAS 28) is not control and generally results in the application of the equity method, rather than consolidation. While IFRS 10 and ASC 810 both base consolidation on control, detailed application (e.g., VIE model under US GAAP) differs; check the applicable framework.

The consolidation process produces the complete set of consolidated financial statements required under IFRS:

- Consolidated statement of financial position (balance sheet): Shows the group’s combined assets, liabilities, and equity after intercompany eliminations.

- Consolidated statement of profit or loss and other comprehensive income (income statement + OCI): Presents group revenue, expenses, profit or loss, and OCI on a unified basis, with intragroup items eliminated in full.

- Consolidated statement of changes in equity: Reconciles opening to closing equity, including share capital, reserves, total comprehensive income, transactions with owners, and movements in non-controlling interests (NCI).

- Consolidated statement of cash flows: Tracks group-wide cash movements across operating, investing, and financing activities.

- Notes to the consolidated financial statements: Sets out significant accounting policies, consolidation principles, key judgments/estimates, and required disclosures.

The Key Starting Point: Trial Balance as Your Foundation

Before diving into complex eliminations, you need rock-solid Trial Balance data from each entity. The Trial Balance is the backbone of your consolidation – if it doesn’t balance at the entity level, your consolidated statements won’t balance either.

Research from leading firms shows that unbalanced Trial Balances are the primary cause of late-night consolidation struggles. Your consolidated Trial Balance should total zero when all debits and credits are properly combined and eliminated.

Key Trial Balance requirements:

- Consistent chart of accounts across all entities

- Same reporting currency (or proper conversion rates applied)

- Matching accounting periods

- All journal entries posted and reviewed

- Sub-ledger reconciliations complete

Step 1: Identify Your Consolidation Scope

Begin by identifying the entities that require consolidation. This isn’t always straightforward – you need to assess control, not just ownership percentages.

Entities Requiring Consolidation

- Subsidiaries where you own >50% voting shares

- Variable Interest Entities (VIEs) where you have a controlling financial interest without majority ownership

- Special Purpose Entities you control through other arrangements

- Subsidiaries you control (control per IFRS 10 not a fixed % threshold)

- VIEs (US GAAP) where you are the primary beneficiary (you have power over the activities that most significantly affect performance and the obligation to absorb losses or right to receive benefits that could be significant)

- Structured/SPE arrangements you control through contractual rights.

You may need to consolidate even if you hold below 50% ownership if you meet IFRS 10’s control test; conversely, at 50% ownership, you may not consolidate if control is joint.

Step 2: Gather Financial Data from All Entities

Collecting accurate, timely financial statements from each subsidiary forms the foundation of your consolidation. This step often reveals the first major challenge: inconsistent reporting formats and accounting policies across entities.

Essential Data to Collect

- Trial Balances with full account detail

- Balance sheets at reporting date

- Income statements for the period

- Cash flow statements

- Supporting schedules for intercompany transactions

- Details of any non-standard transactions

Professional consolidation guidance emphasises that all entities must follow consistent accounting policies. If subsidiaries use different depreciation methods or revenue recognition approaches, you’ll need to adjust these before consolidation.

See how dataSights simplifies the entire consolidation process with automated eliminations, management reports, and direct Excel and Power BI connections in this detailed walkthrough.

Step 3: Convert Foreign Currency (If Applicable)

For multinational groups, currency translation adds another layer of complexity. You’ll need to convert foreign subsidiary statements into your reporting currency using appropriate exchange rates.

Under IAS 21, when translating foreign operations:

- Assets and liabilities are translated at the closing rate at the reporting date

- Income and expenses are translated at exchange rates applicable at transaction dates (with average rates permitted if exchange rates don’t fluctuate significantly)

- All resulting exchange differences are recognised in OCI

Currency translation adjustments flow through other comprehensive income rather than profit and loss, preserving the integrity of your operating results.

Step 4: Eliminate Intercompany Transactions

This is where consolidation becomes complex and where most errors occur. Intercompany eliminations eliminate internal transactions to prevent double-counting and present only external business activities.

Common Eliminations

- Intercompany sales and purchases: When one entity sells to another within your group, both the sale and corresponding purchase must be eliminated.

- Intercompany receivables and payables: Amounts owed between group entities cancel out in consolidation. If Entity A owes Entity B £100,000, this appears as a receivable for B and a payable for A; both must be eliminated.

- Intercompany dividends: Dividends paid from a subsidiary to its parent are considered investment income for the parent but don’t represent external income for the group.

- Intercompany profit in inventory: If one entity sells inventory to another at a markup, and that inventory remains unsold externally, the unrealised profit must be eliminated.

- Intercompany loans and interest: Loans between group entities and related interest charges must be removed from consolidated statements.

Eliminate in full intragroup assets, liabilities, equity, income, expenses and cash flows (including unrealised profits) as required by IFRS 10 B86(c).

Note for Xero users: Xero does not have a native intercompany module; all eliminations and goodwill tracking occur outside of Xero (e.g., in your consolidation/reporting layer). Manual spreadsheet processes across multiple Xero files are the top source of reconciliation errors.

Step 5: Account for Non-Controlling Interests (Minority Interests)

When you own less than 100% of a subsidiary, the portion you don’t own represents non-controlling interest (NCI). This requires careful calculation and presentation in your consolidated statements.

Calculating NCI – A Practical Example

Let’s say Parent Company owns 80% of Subsidiary A:

- Subsidiary A’s net assets: £1,000,000

- Subsidiary A’s profit for the year: £200,000

- NCI ownership: 20%

NCI calculations:

- NCI share of net assets: £1,000,000 × 20% = £200,000

- NCI share of profit: £200,000 × 20% = £40,000

IFRS 3 requires you to measure NCI either at fair value or at the proportionate share of net assets. This choice affects goodwill calculations and subsequent impairment allocations.

The NCI appears as a separate component within equity on your consolidated balance sheet, clearly showing the portion of subsidiary equity not owned by the parent. Allocate NCI after intercompany eliminations. Direction matters: downstream eliminations (parent→sub) reduce the parent’s profit; upstream (sub→parent) reduce the subsidiary’s profit and therefore NCI’s share.

Step 6: Calculate and Record Goodwill

Goodwill arises when you pay more for a subsidiary than the fair value of its identifiable net assets. This premium represents intangible values, like brand reputation, customer relationships, and teamwork.

The Goodwill Formula

Goodwill = Purchase Price + Non-Controlling Interest – Fair Value of Net Assets Acquired

Practical Example

- Purchase price paid: £5,000,000

- Fair value of net assets acquired: £3,500,000

- NCI (if measured at fair value): £500,000

- Goodwill = £5,000,000 + £500,000 – £3,500,000 = £2,000,000

Under current accounting standards, goodwill isn’t amortised but must be tested annually for impairment. If the subsidiary’s value declines, you’ll need to write down goodwill accordingly.

Note for Xero users: Goodwill is recognised under IFRS 3/ASC 805 at acquisition and maintained in the consolidation layer, not in operational ledgers like Xero. Xero does not calculate or track goodwill – record it via consolidation journals.

Step 7: Prepare Consolidated Financial Statements

With eliminations complete and adjustments made, you can now compile your consolidated statements. This involves combining adjusted balances from all entities into unified reports.

Consolidated Balance Sheet Preparation

- Add all asset balances from parent and subsidiaries

- Add all liability balances

- Include parent’s share capital only (not subsidiaries’)

- Calculate consolidated retained earnings (parent’s retained earnings plus share of post-acquisition subsidiary profits)

- Present NCI within equity

- Include goodwill as an intangible asset

Consolidated Income Statement Preparation

- Combine all revenue (less intercompany sales)

- Combine all expenses (less intercompany purchases)

- Calculate consolidated profit

- Allocate profit between parent shareholders and NCI

Financial reporting frameworks require that consolidated statements use uniform accounting policies and cover the same reporting period for all entities.

Regulatory Compliance: IFRS 10 and US GAAP Requirements

Different accounting frameworks have specific consolidation requirements you must follow.

IFRS 10 Key Requirements

- Consolidate all entities you control

- Apply uniform accounting policies

- Use the same reporting date (or within 3 months with adjustments)

- Eliminate all intragroup transactions completely

- Present NCI as part of equity

US GAAP (ASC 810/805) – Key Points

- Two consolidation models: Voting-interest and VIE; consolidate a VIE if you’re the primary beneficiary (power and economics)

- NCI presentation within equity: IFRS 3 allows a measurement election at acquisition (fair value/full goodwill or proportionate share); US GAAP requires fair value for NCI in business combinations. (IFRS 3 PDF) (Deloitte comparison)

- FX: ASC 830 governs US GAAP foreign currency; conceptually similar outcomes to IAS 21 for translation/OCI (not detailed here)

Both frameworks emphasise that control, not just ownership percentage, determines consolidation requirements.

Standard Consolidation Methods and When to Use Them

Understanding different consolidation methods helps you apply the most suitable approach for your specific situation.

Full Consolidation Method

Used when you control the subsidiary (typically >50% ownership). You consolidate 100% of the subsidiary’s assets, liabilities, revenues, and expenses, then show NCI separately for the portion you don’t own.

Equity Method

Applied when you have significant influence but not control (typically 20-50% ownership). Instead of full consolidation, you show your investment as a single line item and recognise your share of the investee’s profits.

Proportional Consolidation

No longer permitted under IFRS or US GAAP since 2013, this method previously allowed consolidating your proportionate share of jointly controlled entities.

Managing Consolidation Adjustments and Journal Entries

Consolidation adjustments ensure your statements accurately reflect the group position. These adjustments are made at the consolidation level, not in individual entity books.

Essential Consolidation Adjustments

- Fair value adjustments: Revaluing subsidiary assets to fair value at acquisition

- Depreciation adjustments: Additional depreciation on fair value uplifts

- Deferred tax adjustments: Tax effects of consolidation adjustments

- Foreign exchange adjustments: Translation differences on foreign operations

- Alignment adjustments: Correcting for different accounting policies

Leading practitioners recommend maintaining detailed documentation of all consolidation adjustments for audit trails and period comparisons.

The Technology Solution: Moving Beyond Manual Excel Consolidation

Manual consolidation in Excel presents significant challenges:

- Error-prone formula links between worksheets

- No audit trail for changes

- Time-consuming data collection

- Difficult to manage multiple currencies

- Complex elimination tracking

- Limited collaboration capabilities

Studies show that 25% of organisations take 10 or more days to close their books using manual processes. Modern consolidation software addresses these challenges through:

- Automated data collection from multiple sources

- Built-in elimination rules

- Real-time currency conversion

- Comprehensive audit trails

- Collaborative processes

- Automatic journal entry generation

For example, dataSights’ Xero consolidation solution automates the entire process – from Trial Balance collection through to board-ready reports. Users report reducing month-end close from over 15 days to under 5 days, with everything balanced and elimination entries fully documented.

Best Practices for Efficient Consolidation

Successful consolidation requires both technical accuracy and efficient processes.

Key Recommendations

- Standardise your chart of accounts across all entities to simplify mapping

- Implement consistent close calendars, ensuring all entities report on schedule

- Document elimination rules for consistency across periods

- Automate data collection to eliminate manual gathering errors

- Perform monthly reconciliations rather than waiting for year-end

- Maintain detailed audit trails for all consolidation adjustments

- Train local teams on consolidation requirements and deadlines

Finance teams spend much of the consolidation cycle on reconciliations and data validation; by standardising data sources, enforcing uniform accounting policies, and automating eliminations and checks, organisations materially reduce errors and shorten the monthly close.

Frequently Asked Questions

What's the Difference Between Consolidated and Combined Financial Statements?

Consolidated financial statements present a parent and its subsidiaries as a single entity, eliminating intercompany transactions. Combined financial statements (often used for entities under common control without a parent) aren’t defined in IFRS; practice is jurisdiction-specific. Many combined presentations still eliminate intra-group transactions/balances to avoid overstatement – disclose policies clearly.

How Long Should Financial Consolidation Take?

Manual consolidation typically takes 10 or more days for most organisations. With proper automation tools, this can be reduced to 3-5 days. The complexity increases with the number of entities, currencies involved, and volume of intercompany transactions.

Do I Need to Consolidate if I Own Exactly 50% of an Entity?

Under IFRS 10 and US GAAP, you consolidate based on control, not just ownership percentage. At 50% ownership, assess whether you have the practical ability to direct relevant activities. If yes, consolidate; if control is shared, apply joint arrangement accounting.

How Do I Handle Different Year-Ends Between Parent and Subsidiary?

IFRS 10.22 allows the use of subsidiary statements with a different reporting date if the gap is no more than three months; adjustments should be made for significant transactions that occurred during the gap.

What if My Trial Balance Doesn't Balance After Consolidation?

An unbalanced consolidated Trial Balance usually indicates missed eliminations or incorrect adjustment entries. Check intercompany account reconciliations first, verify all entities are included, ensure consistent account mapping, and review elimination journal entries for completeness.

Can Consolidation Software Handle Multiple Currencies Automatically?

Yes, modern consolidation platforms like dataSights automatically handle currency conversion using appropriate exchange rates for different statement items. Balance sheet items use period-end rates while income statement items use average rates.

How Do I Track Consolidation Adjustments for Audit Purposes?

Maintain a consolidation adjustments ledger separate from entity books. Document each adjustment with supporting calculations, approvals, and business rationale. Automated systems provide built-in audit trails tracking all changes.

What's the Minimum Ownership Percentage Requiring Consolidation?

There’s no fixed minimum – consolidation depends on control, not ownership percentage. You might consolidate with 40% ownership if you control the entity through other means, or not consolidate at 60% if shareholders’ agreements prevent control.

How Do I Eliminate Intercompany Profit in Inventory?

Calculate the markup on intercompany sales, identify what remains in inventory at period-end, and eliminate the unrealised profit. This adjustment reduces inventory value and consolidated profit until the inventory sells externally.

Should I Consolidate Variable Interest Entities (VIEs)?

Yes, if you’re the primary beneficiary of a VIE, you must consolidate it regardless of ownership percentage. This typically applies to special-purpose entities where you absorb the majority of expected losses or returns.

How Often Should I Test Goodwill for Impairment?

Accounting standards require annual goodwill impairment testing at minimum. Test more frequently if events suggest the carrying value might exceed recoverable amount.

Can Excel Handle Complex Multi-Entity Consolidations Effectively?

While possible, Excel becomes unwieldy with multiple entities, currencies, and eliminations. Formula errors, version control issues, and a lack of audit trails make Excel risky for complex consolidations. Purpose-built software provides better control and efficiency.

Making Consolidation Work for Your Organisation

Financial consolidation doesn’t have to be the dreaded month-end marathon that keeps your finance team working late into the night. With the proper understanding of requirements, clear processes for eliminations and adjustments, and appropriate technology support, you can convert consolidation from a painful necessity into a smooth, controlled process. The key is moving beyond manual Excel-based approaches to embrace automation that handles the complex calculations while maintaining the audit trails and controls that give you confidence in your numbers.

Automate Your Financial Consolidation Today

Stop wrestling with spreadsheets and missed eliminations every month-end. dataSights’ automated consolidation platform handles everything from Trial Balance collection to intercompany eliminations, helping CFOs reduce close time from weeks to days. With proven success across 300+ businesses and 77+ five-star reviews on Xero marketplace, see why finance teams trust dataSights for accurate, efficient consolidation.

About the Author

Kevin Wiegand

Founder & Client happiness

I’m Kevin Wiegand, and with over 25 years of experience in software development and financial data automation, I’ve honed my skills and knowledge in building enterprise-grade solutions for complex consolidation and reporting challenges. My journey includes developing custom solutions for data teams at Gazprom Marketing & Trading and E.ON, before founding dataSights in 2016. Today, dataSights helps over 250 businesses achieve 100% report automation. I’m passionate about sharing my expertise to help CFOs and Financial Controllers reduce their month-end close time and eliminate the manual Excel exports that drain their teams’ valuable time.